Biosimilar Tiers: What They Are and How They Affect Your Prescription Costs

When you hear biosimilar tiers, a system insurance plans use to group similar biologic drugs by cost and coverage rules. Also known as biosimilar formulary levels, it determines how much you pay when your doctor prescribes a drug that copies a brand-name biologic. Unlike regular generics, biosimilars aren’t exact copies—they’re highly similar versions of complex medicines made from living cells, like those used for rheumatoid arthritis, cancer, or diabetes. Because they’re harder to make, their pricing and coverage don’t work like your typical $4 generic pill.

Insurance formularies, lists of drugs covered by a health plan, organized into tiers with different cost-sharing rules. Also known as drug lists, it’s where biosimilar tiers live. Most plans put biosimilars in Tier 2 or 3—lower than the original biologic (often Tier 4), but higher than simple generics (Tier 1). This isn’t random. It’s a strategy: insurers want you to pick the cheaper option, but they still need to make sure the original drug stays available if you need it. Some plans even require you to try the biosimilar first before covering the brand-name version. That’s called a step therapy rule, and it’s common with drugs like Humira or Enbrel.

Why does this matter? Because drug pricing, the cost structure of medications set by manufacturers, insurers, and pharmacies. Also known as pharmaceutical costs, it’s where biosimilar tiers make or break affordability. A biosimilar might cost 30% less than the original, but if your plan puts it in a higher tier, your copay could still be $100. Meanwhile, the brand-name drug might be in a lower tier because the manufacturer pays the insurer a rebate. That’s right—sometimes the more expensive drug costs you less. It sounds backwards, but it’s standard practice. That’s why knowing your tier structure isn’t just helpful—it’s essential. You can’t assume a biosimilar saves you money unless you check your plan’s formulary.

What you’ll find in the posts below is a real-world look at how these systems play out. You’ll see how generic drug competition drives prices down, how older adults question whether biosimilars work as well as the originals, and how pharmacists help patients understand their coverage. You’ll also see how drug safety, patient trust, and insurance rules all connect—not in theory, but in everyday prescriptions. These aren’t abstract policies. They’re the reason someone skips a dose because they can’t afford it, or switches to a new drug because their plan changed. The system isn’t perfect, but understanding biosimilar tiers gives you power over it.

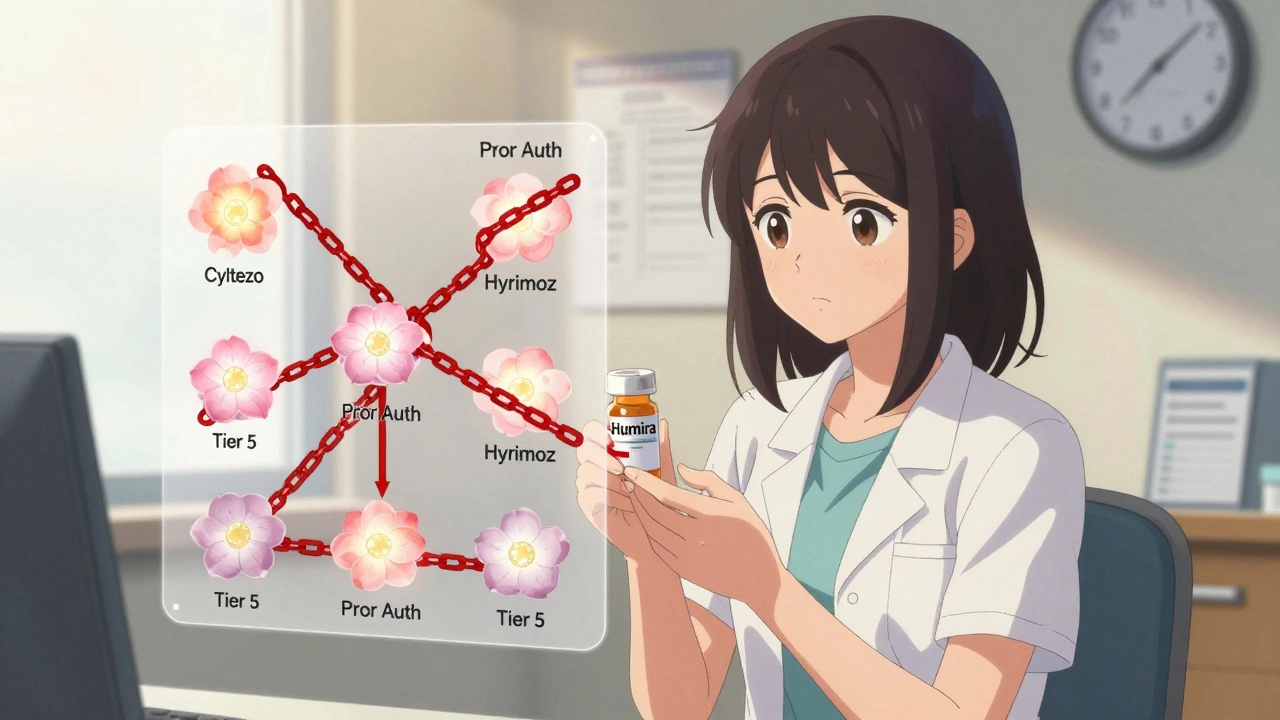

Insurance Coverage of Biosimilars: How Prior Authorization and Tier Placement Block Savings

Despite FDA approval of over 70 biosimilars, most insurance plans still treat them the same as expensive biologics like Humira-same tier, same prior authorization. This blocks savings and delays patient access.

VIEW MORE