Insurance Coverage of Biosimilars: How Prior Authorization and Tier Placement Block Savings

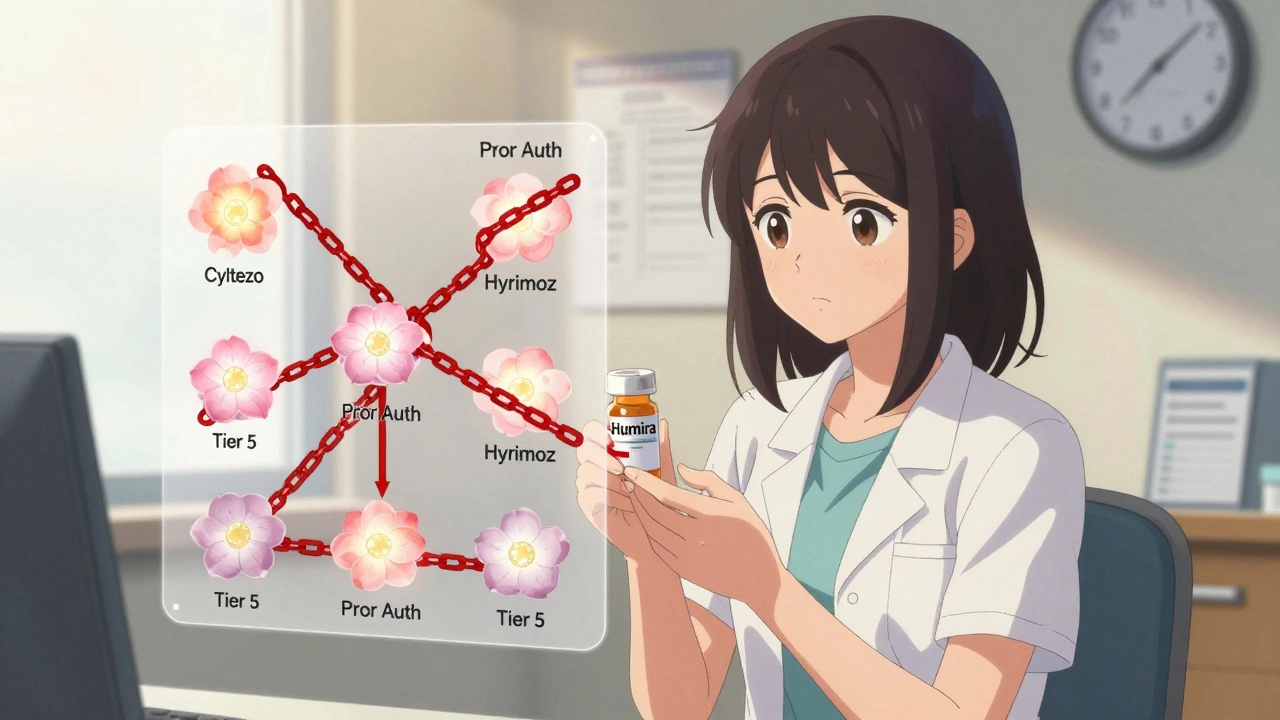

When you’re prescribed a biologic drug like Humira for rheumatoid arthritis or Crohn’s disease, you might expect your insurance to help you save money if a cheaper version becomes available. But here’s the reality: even though there are now eight FDA-approved biosimilars for Humira, most insurance plans still treat them the same as the original drug-no better pricing, no easier access. In fact, in 2025, 99% of Medicare Part D plans put Humira and its biosimilars on the exact same cost tier. That means if you switch from Humira to a biosimilar like Cyltezo or Hyrimoz, your monthly out-of-pocket cost drops by maybe $50-not enough to make a difference for most patients.

Why Biosimilars Are Different From Generics

People often think biosimilars are just like generic pills. They’re not. Generics are exact copies of small-molecule drugs made from chemicals. Biosimilars are made from living cells-think proteins, antibodies, complex molecules. That makes them harder to replicate. The FDA requires them to be “highly similar” to the original biologic, with no clinically meaningful differences in safety or effectiveness. But because they’re so complex, manufacturing them costs millions more than making a generic pill. Still, they’re 10-33% cheaper than the brand-name biologic. That’s why they were created: to bring down prices without sacrificing quality.Here’s the catch: even though biosimilars are cheaper, insurance companies aren’t passing those savings on. In 2024, the average monthly cost for Humira was around $5,000. The biosimilars? Around $4,200. But because they’re on the same tier, patients pay 30% coinsurance either way. That’s $1,500 a month for Humira. $1,260 for the biosimilar. Still a huge burden. And many patients don’t even know they have a cheaper option.

Prior Authorization: The Hidden Gatekeeper

If you want to get a biosimilar, you’ll likely need prior authorization. That means your doctor has to fill out paperwork explaining why you need it, often proving you tried and failed other treatments first. In 2025, 98.5% of insurance plans required prior authorization for both Humira and its biosimilars. Not one plan made it easier for biosimilars. That’s not a coincidence.Some plans even force step therapy: you have to try the biosimilar first, even if your doctor says it’s not right for you. One rheumatologist in Texas told me about a patient with severe RA who waited 28 days to get Humira because her plan required her to fail the biosimilar first. By then, her joints were already damaged. That’s not patient care-that’s cost-shifting disguised as policy.

The process itself is a nightmare. Doctors spend 3-5 hours a week just filling out prior auth forms. Specialty pharmacies get buried under requests. One clinic in Atlanta reported 120 prior auth requests in a single month for biologics alone. That’s 120 hours of staff time. And that’s just for one drug.

Tier Placement: The Real Barrier

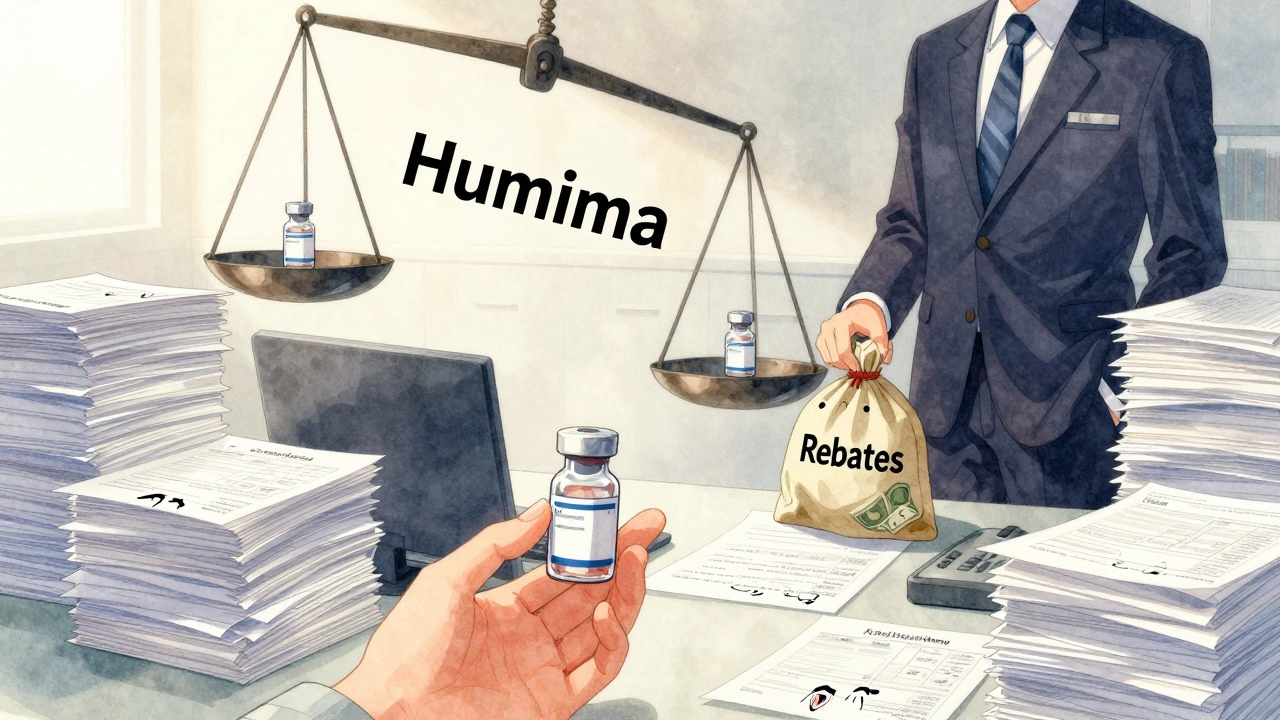

Insurance plans use tiers to control costs. Tier 1 is your $10 generic. Tier 4 or 5? That’s where biologics live. Most plans put Humira and its biosimilars in Tier 5-the highest cost tier. That means you pay a percentage of the drug’s price, not a flat copay. For a $5,000 drug, that’s $1,500 a month. Even if the biosimilar is $4,200, you’re still paying $1,260. No incentive to switch.Here’s the kicker: only 1.5% of plans put biosimilars on a lower tier than the reference product. That’s not just unfair-it’s anti-competitive. The FTC called it out in 2023. PBMs (pharmacy benefit managers) like Express Scripts, OptumRx, and CVS Caremark are the ones setting these rules. They get rebates from drugmakers. And guess what? The original biologic makers pay bigger rebates to stay on the formulary. So even though biosimilars cost less, the PBMs make more money keeping Humira on top.

Some PBMs are starting to flip the script. In 2025, Express Scripts excluded Humira entirely from its national commercial formularies. Instead, they put three biosimilars on Tier 3-preferred specialty-with lower coinsurance. That’s a game-changer. Patients now have no choice but to pick a biosimilar. But this is rare. Most plans still protect the brand.

Why Insurers Resist Change

You might wonder: why don’t insurers just switch everyone to biosimilars? It’s cheaper, right? The answer is money-and power.Biologic manufacturers like AbbVie (maker of Humira) pay huge rebates to PBMs to stay on formularies. Those rebates are hidden from patients and even from insurers. They’re negotiated behind closed doors. So even though a biosimilar might cost $4,200, the PBM gets a $1,000 rebate from AbbVie for every Humira sold. That’s $12,000 a year per patient. That’s not a small incentive to keep the original on the formulary.

Meanwhile, biosimilar makers can’t match those rebates-not yet. They’re still new. They’re still building market share. And they don’t have the same lobbying power. So insurers keep doing what’s profitable, not what’s best for patients.

What’s Changing in 2025?

There’s some progress. The Centers for Medicare & Medicaid Services (CMS) started requiring plans to report biosimilar coverage data in 2024. The results? 78% of Part D plans now cover at least one biosimilar for Humira. That’s up from 50% in 2023. And the Office of Inspector General is watching closely. They warned that if plans keep treating biosimilars worse than the original, it violates the spirit of the Biologics Price Competition and Innovation Act.Some states are stepping in too. California passed a law in 2024 requiring insurers to cover biosimilars without step therapy if the doctor recommends it. Texas is considering something similar. And the Congressional Budget Office says if we fix these barriers, biosimilars could save the U.S. healthcare system $54 billion over the next decade.

But right now, the system is broken. Patients pay more. Doctors waste time. And the real savings? They’re stuck in the middle of a negotiation between drugmakers and PBMs.

What You Can Do

If you’re on a biologic and your insurance won’t cover a biosimilar, here’s what works:- Ask your doctor to write a letter of medical necessity explaining why the biosimilar is appropriate. Mention FDA approval and clinical equivalence.

- Call your insurance company and ask: “Is there a biosimilar on a lower tier? If not, why not?” Get the name of the representative and follow up in writing.

- Check if your plan has a formulary exception process. You can appeal a denial. Many appeals succeed if you have documentation from your doctor.

- Use tools like GoodRx or NeedyMeds to compare cash prices. Sometimes paying out of pocket for the biosimilar is cheaper than your coinsurance.

- Join patient advocacy groups like the Arthritis Foundation or Crohn’s & Colitis Foundation. They’re pushing for policy changes and can help you file complaints.

Don’t accept “that’s just how it is.” You have rights. And you’re not alone. Thousands of patients are stuck in the same situation.

What’s Next?

By 2027, analysts predict biosimilars will make up 40% of the biologics market-if the rules change. But if insurers keep locking them behind prior auth walls and putting them on the same tier as the original? We’ll still be paying $1,500 a month for a drug that could cost half as much.The technology exists. The science is solid. The savings are real. What’s missing is the will to make it fair.

Stacy here

December 8, 2025 AT 04:58Let me tell you something they don’t want you to know - this isn’t about healthcare, it’s about control. The PBMs, the drug giants, the lobbyists - they’re all one big incestuous family. Biosimilars? They’re a threat to the gravy train. You think this is about science? Nah. It’s about who owns your body and how much they can bleed you dry. I’ve seen it. My cousin got denied a biosimilar for 11 months. By then, she needed a wheelchair. They didn’t care. They just wanted their rebates. Wake up.

Wesley Phillips

December 9, 2025 AT 06:38Look I get the outrage but let’s be real - biosimilars aren’t generics. They’re biologics. Complex. Expensive to produce. The fact that they’re 10-33% cheaper is already a win. The real issue is the system’s broken, not the biosimilars. Also, if you’re paying $1500/month out of pocket, you’ve got bigger problems than tier placement. Maybe get a better plan or move to Canada. Just saying.

Kyle Oksten

December 11, 2025 AT 01:18There’s a philosophical layer here that nobody’s talking about. The biologic industry commodifies suffering. It turns chronic illness into a revenue stream with patent extensions, rebates, and tiered formularies. Biosimilars are the first crack in that edifice. But the system doesn’t want cracks - it wants control. So it weaponizes bureaucracy: prior auth, step therapy, tier parity. It’s not incompetence. It’s design. And we’re all just collateral in a market that treats life like a spreadsheet.

Sam Mathew Cheriyan

December 11, 2025 AT 11:38bro why are we even talking about this like its a mystery? its all big pharma and the gubmint they own both. i saw a vid on x where a guy said humira is made from hamster cells?? idk if its true but it sounds right. they just want you hooked and paying forever. biosimilars? nah man theyll never let that fly. its like trying to replace apple with android and apple owns your wifi.

Nancy Carlsen

December 12, 2025 AT 22:07Hey everyone - I’m so glad this post exists. 💛 If you’re reading this and feeling overwhelmed, please know you’re not alone. I’ve been there - crying in the pharmacy parking lot because my copay was $1200. But I fought. I called my rep, got my doc to write a letter, and 3 weeks later, I switched to Cyltezo for $400. It’s possible. You have power. Don’t give up. DM me if you need help navigating this. I’ve got templates. 💪🫶

Ted Rosenwasser

December 13, 2025 AT 23:34Let’s cut the sentimentality. The FDA approved these biosimilars because they’re statistically equivalent. The real villain here isn’t the insurance companies - it’s the patients who don’t understand pharmacoeconomics. You want lower costs? Stop demanding brand-name drugs. Stop being emotionally attached to Humira. It’s a protein. Not a religious icon. Switch. Or stop complaining.

Helen Maples

December 14, 2025 AT 11:46Stop normalizing this abuse. This isn’t just unfair - it’s unethical. Insurance companies are violating the spirit of the BPCIA by design. Your doctor shouldn’t need to spend 5 hours a week filling out forms just so you can get a cheaper, equally safe drug. Document every denial. File complaints with your state insurance commissioner. And if you’re a provider - refuse to participate in step therapy unless it’s clinically justified. This system needs to burn.

David Brooks

December 16, 2025 AT 06:16I used to think this was just a healthcare issue. Then I met a 12-year-old girl on TikTok who injects Humira every other week. Her mom works two jobs. They skipped Christmas last year to afford it. That’s not a statistic. That’s a child. And we’re letting corporations decide if she lives with pain or not. This isn’t about money. It’s about humanity. And we’re failing.

Nicholas Heer

December 17, 2025 AT 15:21THEY’RE FEDERALIZING THE DRUG MARKET TO DESTROY AMERICAN INNOVATION. YOU THINK THIS IS ABOUT HEALTH? NO. IT’S A GLOBALIST SCHEME TO REPLACE OUR MEDICAL SYSTEM WITH CHEAP FOREIGN PRODUCTS. THE PBM’S ARE PART OF THE CRYPTO-BIO-ELITE. THEY WANT YOU DEPENDENT. HUMIRA WAS MADE IN AMERICA. BIOSIMILARS? MADE IN CHINA. WITH LABOR FROM AFGHANISTAN. WE’RE BEING GENTRIFIED OUT OF OUR OWN MEDICINE.

Kyle Flores

December 18, 2025 AT 19:24Hey, I just want to say thank you for writing this. I’ve been on Humira for 7 years. My doc tried switching me to Hyrimoz last year - insurance said no. Took 3 appeals, 2 letters, and a call from my mom to get it approved. It worked. I feel better. No side effects. And I save $300 a month. It’s not perfect, but it’s progress. If you’re struggling - don’t quit. Keep pushing. You’ve got people rooting for you.

Ryan Sullivan

December 19, 2025 AT 02:35Let’s be brutally honest - the entire biologics market is a Ponzi scheme built on regulatory capture. PBMs are middlemen who extract value without adding value. Biosimilars are the logical endpoint of market competition. But the system isn’t designed for competition - it’s designed for rent-seeking. The real tragedy? The public doesn’t even know they’re being fleeced. They think it’s just ‘healthcare costs.’ It’s not. It’s theft.

Olivia Hand

December 20, 2025 AT 00:54Wait - if biosimilars are cheaper and FDA-approved as equivalent, why don’t insurers just switch everyone automatically? Is it really just rebates? Or is there something else? Like… are the biosimilars actually less effective long-term? I’ve heard whispers. Not from docs - from patients. Has anyone seen real data on long-term outcomes? Or is this just fear-mongering?

Desmond Khoo

December 20, 2025 AT 01:37Just switched to Cyltezo last month. My coinsurance dropped from $1400 to $350. My skin cleared up. No new flares. My dog even seems happier. 🐶💙 I didn’t even know I had a choice until I read a Reddit thread. If you’re on Humira and paying through the nose - ask your doc. Ask your insurer. You’re not broken. The system is.